TL;DR Summary

The Net Investment Income Tax (NIIT) is a 3.8% federal surtax applied to investment income — including dividends, capital gains, and rental income — for taxpayers whose Modified Adjusted Gross Income (MAGI) exceeds $200,000 (single) or $250,000 (married filing jointly). Enacted in 2013, the tax now affects 7.3 million Americans and collected $59.8 billion in tax year 2021. It applies on top of regular income and capital gains taxes. Strategic planning — including retirement contributions, tax-loss harvesting, and municipal bonds — can meaningfully reduce or eliminate NIIT exposure. (IRS, 2023; CRS, 2024)

What Is the Net Investment Income Tax (NIIT)?

Who Owes NIIT in 2026?

2026 NIIT Income Thresholds by Filing Status:

| Filing Status | MAGI Threshold | Notes |

|---|---|---|

| Single / Head of Household | $200,000 | Threshold unchanged since 2013 |

| Married Filing Jointly | $250,000 | Threshold unchanged since 2013 |

| Married Filing Separately | $125,000 | Half of MFJ threshold |

| Qualifying Widow(er) | $250,000 | Same as MFJ |

| Estates & Trusts | $16,000 (AGI) | Indexed for inflation; was $15,650 in 2025 |

What Income Is Subject to NIIT?

Net investment income (NII) includes passive income from financial assets. The following are included:

- Interest income (savings accounts, CDs, bonds)

- Dividends (both qualified and ordinary)

- Capital gains (short-term and long-term)

- Rental and royalty income (passive)

- Non-qualified annuity distributions

- Passive business income (limited partnerships, S-corps with passive participation)

The following income types are excluded from NIIT:

- Wages, salaries, and self-employment income

- Social Security benefits

- Distributions from qualified retirement plans (401(k), IRA, 403(b))

- Tax-exempt municipal bond interest

- Veterans Administration benefits

- Home sale gains excluded under Section 121 ($250K single / $500K joint)

Important for real estate investors and business owners: passive rental income and K-1 passive income are subject to NIIT even though they may feel like ‘earned’ income. Active participation and real estate professional status can change this classification. (IRS, 2026; KLR, 2026)

NIIT vs. Other Investment Taxes: Key Comparisons

| Tax | Rate | Who It Applies To | Income Type |

|---|---|---|---|

| Net Investment Income Tax (NIIT) | 3.8% | MAGI > $200K/$250K | Investment income only |

| Long-Term Capital Gains Tax | 0%, 15%, or 20% | All taxpayers | Assets held > 1 year |

| Short-Term Capital Gains Tax | Ordinary rate (up to 37%) | All taxpayers | Assets held < 1 year |

| Additional Medicare Tax | 0.9% | Wages > $200K/$250K | Wages/self-employment only |

| Ordinary Income Tax | 10%–37% | All taxpayers | Most income types |

How Is NIIT Calculated?

Step-by-Step NIIT Calculation:

- Determine your MAGI (usually equals your AGI on Form 1040).

- Identify your filing status threshold ($200K single / $250K MFJ).

- Calculate the excess: MAGI minus threshold = Excess MAGI.

- Calculate your total Net Investment Income (NII).

- Apply 3.8% to the lesser of: NII or Excess MAGI.

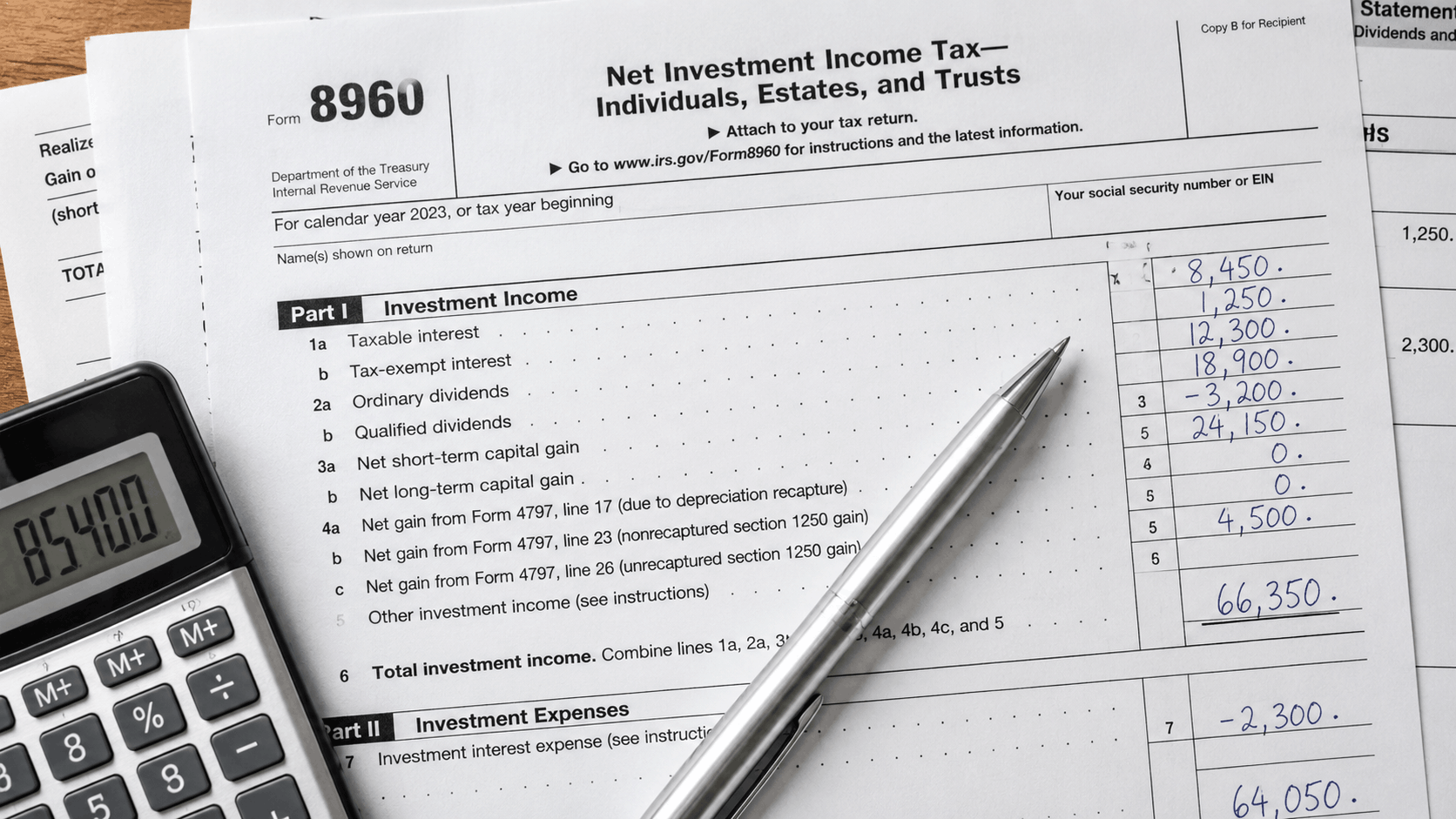

- Report the result on IRS Form 8960 and attach to Form 1040.

7 Strategies to Reduce Your NIIT in 2026

Because the NIIT thresholds are not indexed for inflation, proactive planning is increasingly important. Here are the most effective strategies:

1. Maximize Pre-Tax Retirement Contributions

2. Tax-Loss Harvesting

2. Tax-Loss Harvesting

3. Time Capital Gains Across Tax Years

4. Invest in Municipal Bonds

5. Roth Conversions and Withdrawal Planning

6. Use 1031 Exchanges for Real Estate

7. Donate Appreciated Securities

Donating appreciated stock or mutual fund shares directly to a charity avoids capital gains recognition entirely, removing those gains from both your NII and MAGI. The donor also receives a charitable deduction equal to the fair market value. Note that charitable contributions are not deductible against NII for NIIT purposes, but eliminating the gain itself is the key benefit. (Wealth Enhancement, 2026)

NIIT and Estates & Trusts

Estates and trusts face NIIT at a much lower AGI threshold than individuals — just $16,000 in 2026 (up from $15,650 in 2025). This means most non-exempt trusts holding investment assets will owe NIIT on undistributed investment income. One planning strategy: distribute investment income to beneficiaries who fall below the individual NIIT thresholds. Charitable remainder trusts (CRTs), grantor trusts, and perpetual care trusts are exempt from NIIT. (Fidelity, 2026; Ameriprise, 2026)

The Growing Reach of NIIT: Why More Taxpayers Are Affected

The NIIT thresholds — $200,000 for single filers, $250,000 for married couples — have not changed since the tax was enacted in 2013. Because they are not indexed for inflation, a growing number of Americans cross these thresholds each year even if their real purchasing power has not meaningfully increased. The number of NIIT payers grew from 3.1 million in 2013 to 7.3 million in 2021 (IRS, 2023), and NIIT revenue rose from $16.5 billion to $59.8 billion over the same period (Congressional Research Service, 2024). The Congressional Budget Office projects NIIT revenue will reach $67 billion by 2034.

Frequently Asked Questions

1. Does the net investment income tax apply to rental income?

Yes. Passive rental income is subject to the 3.8% NIIT if your MAGI exceeds the threshold. However, if you qualify as a real estate professional under IRS rules — meaning you spend more than 750 hours per year in real estate activities and it constitutes more than half your working time — your rental income may be considered active, not passive, and could be exempt from NIIT. (IRS, 2026)

2. Is Social Security subject to NIIT?

No. Social Security benefits are not classified as net investment income and are not subject to the 3.8% NIIT. However, Social Security benefits that are included in your gross income do count toward your MAGI, which can indirectly push you over the NIIT threshold and trigger the tax on other investment income. (IRS, 2026)

3. Do 401(k) or IRA distributions trigger NIIT?

No. Distributions from qualified retirement accounts — including traditional 401(k)s, IRAs, 403(b)s, and 457(b)s — are not classified as net investment income. However, they do increase your MAGI, which could push you over the NIIT threshold and cause your other investment income to be taxed at 3.8%. (Fidelity, 2026)

4. Are capital gains from selling my home subject to NIIT?

Only partially. The Section 121 exclusion shields the first $250,000 of home sale gain (single) or $500,000 (married filing jointly) from both regular income tax and NIIT. Any gain above those exclusion limits is considered net investment income and may be subject to the 3.8% surtax if your MAGI exceeds the threshold. (IRS, 2026)

5. Can I reduce NIIT by investing in municipal bonds?

Yes, this is one of the most straightforward NIIT reduction strategies. Interest from municipal bonds is excluded from both MAGI and net investment income, making it invisible to the NIIT calculation. Shifting taxable bond holdings to tax-exempt munis reduces both your income base and your potential NII. (KLR, 2026)

6. Is the NIIT rate going up in 2026 or beyond?

The NIIT rate of 3.8% has remained unchanged since 2013 and was not altered by the One Big Beautiful Bill Act signed in July 2025. While proposals to expand or raise the NIIT have been discussed at the federal level, no changes are currently law for 2026. (Kiplinger, 2026)

7. What form do I use to report NIIT?

Individuals calculate and report NIIT using IRS Form 8960, Net Investment Income Tax — Individuals, Estates, and Trusts. The completed form is attached to Form 1040 (individuals) or Form 1041 (estates and trusts). If your income is near the threshold, proactively increasing withholding or making estimated quarterly payments via Form 1040-ES can prevent underpayment penalties. (IRS, 2026)

Works Cited

Congressional Research Service. “The 3.8% Net Investment Income Tax: Overview, Data, and Policy Options.” Congress.gov. 2024. https://www.congress.gov/crs-product/IF11820

Internal Revenue Service. “Net Investment Income Tax.” IRS.gov. 2026. https://www.irs.gov/individuals/net-investment-income-tax

Internal Revenue Service. “Topic No. 559: Net Investment Income Tax.” IRS.gov. February 2026. https://www.irs.gov/taxtopics/tc559

Fidelity Investments. “What Is Net Investment Income Tax (NIIT)?” Fidelity.com. March 2026. https://www.fidelity.com/learning-center/trading-investing/net-investment-income-tax

KLR (Kahn Litwin Renza). “Maximizing Tax Efficiency in 2026: Understanding the NIIT.” KahnLitwin.com. April 2026. https://kahnlitwin.com/blogs/tax-blog/maximizing-tax-efficiency-in-2026-understanding-the-niit

Ameriprise Financial. “The Net Investment Income Tax: What It Is and How to Potentially Minimize It.” Ameriprise.com. 2026. https://www.ameriprise.com/financial-goals-priorities/taxes/net-investment-income-tax

Urban Institute. “Net Investment Income Tax: A Primer.” Urban.org. January 2025. https://www.urban.org/sites/default/files/2025-01/Net%20Investment%20Income%20Tax.pdf

ITEP (Institute on Taxation and Economic Policy). “The Wealth Proceeds Tax.” ITEP.org. January 2026. https://itep.org/wealth-proceeds-tax-net-investment-income-tax/

Wealth Enhancement Group. “Net Investment Income Tax (NIIT): What It Is, Who Pays It, and How to Plan.” WealthEnhancement.com. 2026. https://www.wealthenhancement.com/blog/what-is-net-investment-income-tax-how-can-you-plan-for-it

Kiplinger. “Capital Gains Tax Rates 2025 and 2026.” Kiplinger.com. April 2026. https://www.kiplinger.com/taxes/capital-gains-tax/602224/capital-gains-tax-rates