TL;DR Summary

The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, permanently raised the federal estate and gift tax exemption to $15 million per individual ($30 million per married couple) effective January 1, 2026. For high-net-worth families, the scramble to beat an arbitrary sunset deadline is over — but the planning imperative is not. Families with estates exceeding the exemption threshold still face a 40% tax on the overage, and $124 trillion in intergenerational wealth will change hands through 2048. The strategies that now matter most are irrevocable trusts (GRATs, IDGTs, SLATs), dynasty trusts, family governance frameworks, and charitable vehicles. This guide covers every major tool, with a step-by-step action checklist.

1. The 2026 Tax Landscape for High-Net-Worth Families

The most consequential estate planning development in decades came on July 4, 2025, when President Trump signed the One Big Beautiful Bill Act (OBBBA) — One Big Beautiful Bill Act — the sweeping tax legislation that replaced the temporary Tax Cuts and Jobs Act (TCJA) provisions with permanent law. For wealthy families, it ended years of planning uncertainty.

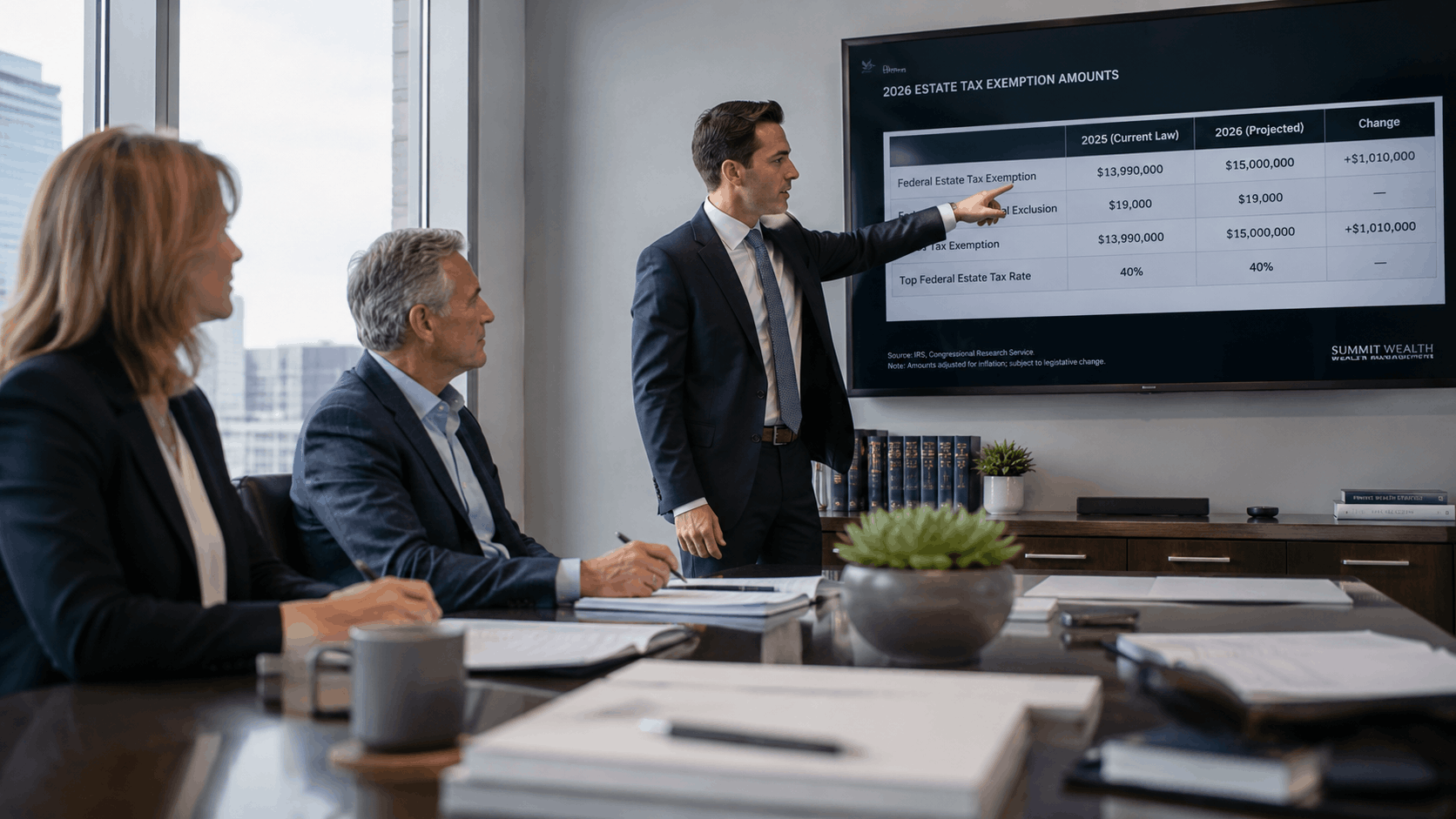

Key 2026 Federal Numbers at a Glance:

| Tax Provision | 2025 Amount | 2026 Amount (OBBBA) |

|---|---|---|

| Estate & Gift Tax Exemption (Individual) | $13.99 million | $15 million |

| Exemption (Married Couple) | $27.98 million | $30 million |

| Annual Gift Tax Exclusion | $18,000 per recipient | $19,000 per recipient |

| GST (Generation-Skipping Transfer) Exemption | $13.99 million | $15 million |

| Top Estate Tax Rate (over exemption) | 40% | 40% (unchanged) |

| Inflation Indexing | N/A (was set to sunset) | Yes, beginning 2027 (base year: 2025) |

| Sunset Provision | Scheduled to drop ~50% | None — permanent law |

Answer Block: What Did the OBBBA Change for Estate Taxes?

The One Big Beautiful Bill Act (OBBBA) — landmark federal legislation signed July 4, 2025 — permanently set the federal estate, gift, and GST tax exemption at $15 million per individual ($30 million for married couples), effective January 1, 2026. Unlike the 2017 Tax Cuts and Jobs Act (TCJA), the OBBBA carries no automatic expiration date. The exemption will be indexed for inflation annually from 2027 onward, using 2025 as the base year. (IRS Revenue Procedure 2025-32, 2025)

Important nuance: While the OBBBA removes the scheduled sunset, future Congresses can still amend the law. Estate planning attorneys widely advise families not to interpret “permanent” as “forever” — proactive planning within the next several years remains essential before political or legislative winds shift. (Pierce Atwood, 2025)

2. Who Needs Advanced Estate Planning in 2026?

Not every wealthy family faces the same planning calculus. The $15 million individual exemption means that for unmarried individuals with estates below that threshold, federal estate tax is no longer the primary concern — though state-level estate taxes in 18 states and jurisdictions remain significant considerations.

For families whose combined net worth exceeds $30 million — or who anticipate meaningful asset appreciation — the planning conversation shifts from “will we owe estate tax?” to “how do we maximize what passes to the next generation?” This is the group for whom the strategies in this guide are most relevant.

The stakes are massive at a macro level: according to projections by Cerulli Associates, approximately $124 trillion in wealth will change hands through 2048 — with $105 trillion flowing to heirs and $18 trillion to charities (Cerulli Associates, U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2024). Critically, more than 50% of that total ($62 trillion) will come from high-net-worth and ultra-high-net-worth households, which together represent just 2% of all U.S. households. Planning wisely now determines how much of that wealth survives the transfer — and on whose terms.

3. Advanced Wealth Transfer Strategies for HNW Families

Grantor Retained Annuity Trust (GRAT)

| GRAT Feature | Detail |

|---|---|

| Ideal for | Assets expected to appreciate rapidly (private equity, pre-IPO stock, real estate) |

| Term | Typically 2–10 years; shorter terms reduce mortality risk |

| IRS hurdle rate | Section 7520 rate (April 2026 rate: check IRS monthly update) |

| Gift tax consequence | Near-zero gift tax if assets appreciate above hurdle rate |

| Risk | Grantor must survive the trust term; assets returned if they underperform |

| Advanced tactic | Rolling short-term GRATs ("zeroed-out GRATs") on different asset classes |

Intentionally Defective Grantor Trust (IDGT)

An Intentionally Defective Grantor Trust (IDGT) — a trust that is treated as outside the grantor’s estate for estate tax purposes but as “owned” by the grantor for income tax purposes — is the premier estate-freeze tool for ultra-high-net-worth families. Assets sold to the IDGT lock in today’s value for estate tax purposes, while all future appreciation occurs outside the taxable estate.

The “defect” is intentional: specific trust provisions (such as a swap power allowing the grantor to exchange assets of equal value) cause the IRS to treat the grantor as the income tax owner, meaning: (1) no capital gains tax is triggered on the sale of assets to the trust, and (2) the grantor’s payment of income taxes on trust earnings is effectively an additional annual gift to the trust beneficiaries — made without consuming any gift tax exemption. (Peak Trust, 2026)

For business owners, the IDGT is especially powerful: transferring closely held business interests at today’s valuation means decades of future appreciation compound entirely outside the taxable estate. When structured as a dynasty trust (see below), the compounding can benefit multiple generations.

Spousal Lifetime Access Trust (SLAT)

Answer Block: What Is a SLAT and Why Is It So Popular in 2026?

A Spousal Lifetime Access Trust (SLAT) — an irrevocable trust created by one spouse for the benefit of the other, removing assets from the donor spouse’s taxable estate while preserving the couple’s indirect access to the funds via the beneficiary spouse — has become the go-to strategy for couples in 2026. Under the OBBBA’s $15 million exemption, one spouse can transfer up to that amount into a SLAT, locking in the value and removing all future appreciation from both spouses’ estates. The beneficiary spouse can receive distributions, providing a financial safety valve. (Fidelity Investments, 2026; Fiduciary Trust, 2026)

Critical SLAT considerations:

- No step-up in basis: Assets in a SLAT do not receive a step-up in cost basis at death, potentially creating capital gains tax liability that partially offsets estate tax savings.

- Reciprocal trust doctrine: If both spouses create SLATs for each other, the trusts must be sufficiently different to avoid IRS recharacterization.

- Divorce or death risk: If the beneficiary spouse dies first or a divorce occurs, the donor spouse loses indirect access to the trust assets.

- Community property states: Extra documentation (transmutation agreements) is required in the nine community property states.

Dynasty Trust

A dynasty trust — an irrevocable trust designed to hold assets for multiple generations, often 100+ years in trust-friendly states — allows families to allocate their $15 million GST exemption once and let wealth compound entirely outside the transfer tax system for generations. Unlike assets passed outright at each generational death (subject to estate tax each time), assets inside a properly funded dynasty trust can pass from grandparents to children to grandchildren to great-grandchildren without triggering estate or GST tax at each transfer. (Charles Schwab, 2024)

- Best states for dynasty trusts: South Dakota, Nevada, and Delaware — offering no state income tax on trust earnings, favorable decanting laws, and perpetual (or near-perpetual) trust durations.

- Dynasty trusts also provide creditor protection and shield assets from beneficiaries’ divorces or lawsuits.

- An IDGT structured as a dynasty trust is considered the pinnacle of multigenerational planning for UHNW families.

4. Charitable Vehicles: Philanthropy as a Planning Strategy

| Vehicle | How It Works | Best For |

|---|---|---|

| Charitable Remainder Trust (CRT) | Grantor transfers appreciated assets; CRT sells them tax-deferred. Grantor receives income for life or a term. Charity receives the remainder. | Diversifying out of concentrated positions; retirement income planning. |

| Charitable Lead Trust (CLT) | Charity receives income for a set term (the "lead" interest). Remainder passes to heirs, often at a substantially reduced taxable value. | Reducing the taxable value of gifts to children; high-income years when charitable deductions are most valuable. |

| Donor-Advised Fund (DAF) | Grantor makes an irrevocable contribution, takes an immediate income tax deduction, and recommends grants over time. | Flexible charitable giving; concentrating deductions in high-income years. |

| Private Foundation | Family-controlled entity that makes grants. Subject to IRS excise tax and distribution requirements. | Families seeking long-term philanthropic legacy and control over giving. |

5. Family Governance and the Family Office Model

As wealth grows, financial complexity eventually outpaces what a network of individual advisors can manage. The answer for UHNW families is governance infrastructure — formal structures that coordinate investment management, tax planning, estate administration, succession, and family communication.

Answer Block: What Is a Family Office and When Does Your Family Need One?

A family office is a dedicated private organization — either a Single-Family Office (SFO) serving one family or a Multi-Family Office (MFO) serving multiple families — that provides comprehensive, integrated wealth management: investment oversight, estate and tax planning, succession coordination, philanthropy, and family governance. SFOs typically become cost-effective at wealth levels above $100–$250 million. MFOs provide institutional-quality services at lower cost, making them appropriate for families in the $20–$100 million range. According to the J.P. Morgan 2026 Global Family Office Report — a survey of 333 family offices across 30 countries averaging $1.6 billion in net worth — 86% of family offices globally lack a clear succession plan for key decision-makers. (J.P. Morgan Private Bank, 2026)

Key Governance Tools:

- Family Constitution: A formal document outlining the family’s mission, values, and rules governing how wealth is accessed by future generations — including qualifications for distributions, family employment policies, and conflict resolution mechanisms.

- Investment Policy Statement (IPS): Defines asset allocation targets, liquidity buckets, concentration limits, and spending policies for the family office.

- Family Council: A regular meeting structure that brings family members together for governance education, communication, and decision-making — critical for preventing the conflicts that the J.P. Morgan report identifies as a top-3 risk for family offices.

- Succession Plan: Per the J.P. Morgan 2026 report, 33% of family offices cite lack of a succession plan for key decision-makers as a primary risk to long-term effectiveness. Formalizing leadership transition — both for the family and the office staff — is essential.

6. 2026 Estate Planning Action Checklist for HNW Families

This checklist is organized by urgency. Items in Phase 1 should be completed within the next 90 days; Phase 2 within 12 months.

Phase 1 — Immediate Review (90 Days)

- Review all existing trust documents for language that references the federal estate tax exemption by dollar amount — the OBBBA’s increase to $15M may inadvertently trigger unintended distributions. (Paoli Law, 2025)

- Conduct a step-up-in-basis audit: Identify assets best held until death (to receive a step-up in capital gains cost basis) versus assets better suited to gift now (to remove future appreciation from the estate).

- Confirm your state’s estate tax rules: 18 states and jurisdictions impose estate or inheritance taxes with much lower exemptions than the federal $15M threshold. Minnesota, for example, has a state estate tax.

- Verify beneficiary designations on all retirement accounts, life insurance, and transfer-on-death accounts — these pass outside of trusts and wills.

Phase 2 — Strategic Implementation (12 Months)

- Model a SLAT if your estate, with appreciation projections, will exceed $30M combined. Evaluate which spouse should be the donor based on asset composition and community property rules.

- Evaluate GRATs for rapidly appreciating assets — particularly private equity, pre-IPO stock, and real estate in high-growth markets.

- Consider establishing a dynasty trust in a favorable jurisdiction (South Dakota, Nevada, or Delaware) and funding it with your available GST exemption.

- Review your charitable giving strategy under OBBBA’s new floor and cap on itemized charitable deductions.

- Establish or update a formal succession plan for closely held business interests, including buy-sell agreements and current independent valuations.

- Evaluate whether your current advisory structure (individual advisors vs. multi-family office) can adequately coordinate across tax, legal, investment, and governance functions.

7. How 'Permanent' Is Permanent? Planning Under Legislative Uncertainty

Despite widespread use of the word “permanent,” the OBBBA’s $15 million exemption is only permanent until Congress acts otherwise. The 2017 TCJA also appeared durable — and was on course to be cut in half just 8 years later. Estate planning attorneys from Pierce Atwood to BNY Mellon broadly advise that families should use the next two to three years to implement foundational planning strategies, particularly GRATs, SLATs, and dynasty trusts funded with GST exemption, before a potential change in congressional control. (Pierce Atwood, 2025; BNY Mellon, 2026)

Frequently Asked Questions

1. What is the federal estate tax exemption for 2026?

The One Big Beautiful Bill Act set the federal estate and gift tax exemption at $15 million per individual and $30 million for married couples, effective January 1, 2026. The exemption is indexed for inflation beginning in 2027 and has no automatic expiration date, though future Congress may change it. (IRS, 2025)

2. Does a high net worth family still need estate planning if they are under $30 million?

Yes. Eighteen states and jurisdictions impose their own estate or inheritance taxes with much lower exemptions. Additionally, families just below the $30M threshold today may cross it through investment appreciation over time. Asset protection, governance, and succession planning benefits apply at all wealth levels.

3. What is the difference between a GRAT and an IDGT?

A GRAT is designed to transfer appreciation on specific assets over a fixed term, with the grantor retaining an annuity payment. An IDGT is an estate-freeze vehicle where the grantor sells assets to the trust in exchange for a promissory note — locking in the current value for estate tax purposes while all future appreciation grows outside the estate. The grantor pays income taxes on the trust’s earnings, constituting an additional tax-free gift to beneficiaries.

4. Is a Spousal Lifetime Access Trust (SLAT) still a good strategy now that the exemption is $15M?

Yes. A SLAT allows one spouse to use their full $15M exemption to remove assets — plus all future appreciation — from both spouses’ estates, while the beneficiary spouse retains access to distributions. Given that estates exceeding $30M still face a 40% estate tax on the excess, and that the $15M exemption could be reduced by a future Congress, SLATs remain one of the most valuable planning tools for HNW couples. (Fidelity Investments, 2026)

5. What is a dynasty trust and do we need one?

A dynasty trust is an irrevocable trust designed to hold family wealth for multiple generations — often 100+ years in trust-friendly states like South Dakota, Nevada, or Delaware — passing assets without triggering estate or generation-skipping transfer taxes at each generational transition. Families allocate their $15M GST exemption to fund the trust, and all future growth benefits multiple generations tax-efficiently. It is most powerful for UHNW families whose wealth will significantly exceed exemption levels.

6. When should a high-net-worth family consider a family office?

A single-family office typically becomes cost-effective for families with $100M+ in investable assets. Multi-family offices serve families in the $20–$100M range effectively. The key trigger is not just wealth level but complexity: multiple trusts, a closely held business, properties in multiple states or countries, charitable vehicles, and multiple generations with differing needs all point toward a dedicated coordination structure.

7. What are the 18 states that have their own estate or inheritance taxes in 2026?

As of 2026, states and jurisdictions with their own estate or inheritance taxes include: Connecticut, Hawaii, Illinois, Iowa, Kentucky, Maine, Maryland, Massachusetts, Minnesota, Nebraska, New Jersey, New York, Oregon, Pennsylvania, Rhode Island, Vermont, Washington, and Washington D.C. Minnesota, for example, has a state estate tax exemption significantly below the federal $15M threshold, making state-level planning critical for residents. Consulting a state-specific estate planning attorney is strongly advised.

Works Cited

BNY Mellon Wealth Management. “Q&A: How the One Big Beautiful Bill’s $15M Estate Exemption Reshapes Multigenerational Giving.” BNY.com. March 30, 2026. https://www.bny.com/wealth/global/en/insights/qa-how-the-one-big-beautiful-bills-15m-estate-exemption-reshapes-multigenerational-giving.html

Cerulli Associates. “The Cerulli Report—U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2024: The Great Wealth Transfer.” December 2024.

Fidelity Investments. “What Is the One Big Beautiful Bill Act and What Does It Mean for Me?” Fidelity.com. October 2025. https://www.fidelity.com/learning-center/personal-finance/one-big-beautiful-bill

Fidelity Investments. “Protect Assets with a SLAT.” Fidelity.com. January 2026. https://www.fidelity.com/learning-center/wealth-management-insights/protect-assets-with-a-SLAT

Fiduciary Trust. “Spousal Lifetime Access Trusts: Are They All They’re Cracked Up To Be?” Fiduciary-Trust.com. January 2026. https://www.fiduciary-trust.com/insights/spousal-lifetime-access-trusts/

Harter Secrest & Emery LLP. “2026 Outlook: The One Big Beautiful Bill Act, Permanent Estate Tax Exemptions, and SALT Deduction Changes.” HSELaw.com. December 2025.

Internal Revenue Service. “IRS Releases Tax Inflation Adjustments for Tax Year 2026, Including Amendments from the One, Big, Beautiful Bill.” IRS.gov. October 2025. https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

J.P. Morgan Private Bank. “2026 Global Family Office Report.” JPMorgan.com. February 2026. https://privatebank.jpmorgan.com/nam/en/insights/reports/2026-family-office-report

Morgan Lewis. “Estate Tax Alert: New $15 Million Federal Exemption Becomes Law.” MorganLewis.com. August 2025. https://www.morganlewis.com/pubs/2025/08/estate-tax-alert-new-15-million-federal-exemption-becomes-law

Peak Trust Company. “What Is an Intentionally Defective Grantor Trust.” PeakTrust.com. January 2026. https://peaktrust.com/what-is-an-intentionally-defective-grantor-trust/

Pierce Atwood LLP. “The One Big Beautiful Bill Act and Estate Planning: What You Need to Know.” PierceAtwood.com. 2025. https://www.pierceatwood.com/alerts/one-big-beautiful-bill-act-and-estate-planning-what-you-need-know

Porter Simon. “Spousal Lifetime Access Trusts (SLATs): Advantages, Pitfalls, and a 2026 Planning Guide.” PorterSimon.com. March 2026.