TL;DR Summary

The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, permanently raised the federal estate tax exemption to $15 million per individual ($30 million per married couple) effective January 1, 2026. The feared ‘sunset cliff’ that would have halved exemptions is gone. For high-net-worth families, the planning priority has shifted from emergency gifting to long-term optimization: deploying IDGTs to freeze appreciating assets, using SLATs to maintain indirect access to transferred wealth, building dynasty trusts to protect generational transfers from GST tax, and strategically managing exposure to state-level estate taxes — which remain a serious risk in 12 jurisdictions including New York, Oregon, and Massachusetts.

Why 2026 Is a Turning Point for Estate Planning

For years, the dominant theme in estate planning was urgency: use your elevated exemption before the Tax Cuts and Jobs Act sunset kicked in and cut it roughly in half. That anxiety is now off the table. The passage of the One Big Beautiful Bill Act (OBBBA) — signed by President Trump on July 4, 2025 — permanently codified a $15 million federal exemption, indexed for inflation starting in 2027 (IRS, 2025).

But permanent does not mean permanent forever. As estate attorneys at Pierce Atwood noted after the bill’s passage, a future Congress could always change the law. Families have a window of stability — and they should use it wisely. For those with estates above $15 million (or $30 million per couple), the 40% rate still applies to every dollar over the threshold, and state taxes create a second layer of exposure that millions of families overlook.

Answer Block:

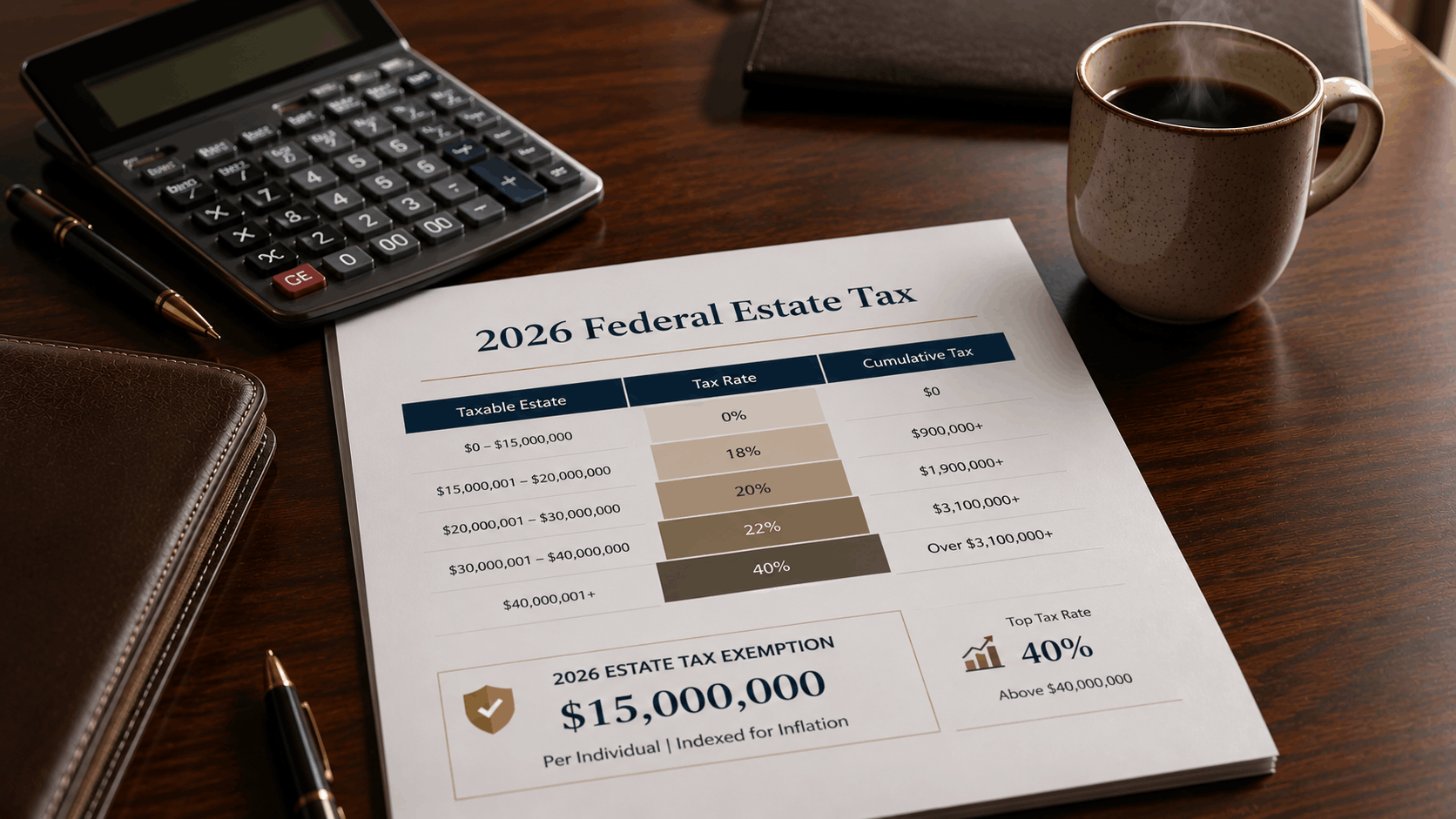

The One Big Beautiful Bill Act (OBBBA) — federal legislation signed July 4, 2025 — permanently increased the U.S. federal estate, gift, and generation-skipping transfer tax exemption to $15 million per individual ($30 million for married couples) effective January 1, 2026. The exemption is inflation-indexed starting in 2027. The top federal estate tax rate remains 40% on amounts exceeding the exemption.

2026 Federal Estate Tax: Key Numbers at a Glance

Before diving into strategy, every high-net-worth family needs to internalize the current numbers. The table below summarizes the critical thresholds for 2026.

| Category | 2026 Limit | Key Notes |

|---|---|---|

| Individual Federal Exemption | $15,000,000 | Up from $13.99M in 2025; permanent, inflation-indexed from 2027 |

| Married Couple Exemption | $30,000,000 | Requires portability election or bypass trust planning |

| Top Federal Estate Tax Rate | 40% | Applied to amounts above the exemption threshold |

| Annual Gift Tax Exclusion | $19,000/recipient | $38,000 for married couples using gift-splitting |

| GST Tax Exemption | $15,000,000 | Matches estate exemption; NOT portable between spouses |

| Non-U.S. Citizen Spouse Annual Gift | $194,000 | Up from $190,000 in 2025 (IRS, 2025) |

| 5-Year 529 Gift Acceleration | $95,000 individual / $190,000 couple | Per grandchild; front-loads annual exclusions (Fidelity, 2026) |

Strategy 1: The Estate Freeze — Intentionally Defective Grantor Trusts (IDGTs)

How an IDGT Works — Step by Step

- Create an irrevocable trust with a ‘grantor trust’ trigger built in (e.g., a power to substitute assets of equivalent value).

- Make a ‘seed gift’ of at least 10% of the assets to be sold — typically cash or liquid securities — to give the trust the economic substance of a real buyer.

- Sell the target asset (often a closely-held business interest, real estate, or concentrated stock position) to the trust at fair market value in exchange for a promissory note.

- The note’s interest rate must equal at least the IRS Applicable Federal Rate (AFR) for the term selected. Short-term: 3 years or less; mid-term: 3–9 years; long-term: over 9 years.

- The grantor pays income taxes on trust income out of personal assets — a non-gift tax depletion of the taxable estate, often called ‘bonus gifting.’

- If the trust’s assets appreciate faster than the AFR, all excess growth passes to heirs completely free of estate and gift tax.

The Core Bet: The IDGT only wins if the transferred asset appreciates faster than the AFR. High-growth assets — a pre-IPO equity stake, an appreciating commercial property, a family business — are ideal candidates. Placing slow-growth or depreciating assets is counterproductive: you may receive back more in note payments than the asset is worth (RSM, 2024).

Answer Block:

An Intentionally Defective Grantor Trust (IDGT) is an irrevocable trust used in estate planning that is ‘defective’ for income tax purposes — meaning the grantor pays income tax on trust earnings — but fully effective for estate and gift tax purposes, removing assets from the taxable estate. Assets are typically sold to the IDGT via an installment note at the IRS Applicable Federal Rate (AFR), freezing the estate value and shifting future appreciation to heirs tax-free. This makes IDGTs particularly effective for high-growth assets held by high-net-worth families.

Key Risk: The IDGT structure requires the grantor to have sufficient personal income or assets to sustain ongoing income tax payments on the trust’s earnings without dipping into the trust itself. Consult qualified estate counsel before proceeding (Fidelity, 2026).

Strategy 2: Access Without Ownership — Spousal Lifetime Access Trusts (SLATs)

Even with a $15 million exemption, many high-net-worth individuals face a psychological and practical hurdle: making a large, irrevocable gift feels like permanently surrendering control. A Spousal Lifetime Access Trust (SLAT) solves that problem by allowing one spouse — the donor spouse — to fund an irrevocable trust for the benefit of the other spouse, removing assets from the gross estate while maintaining indirect household access through the beneficiary spouse (Schwab, 2026).

SLAT Benefits at a Glance

- Removes assets (and all future appreciation) from the donor spouse’s taxable estate immediately upon funding

- Beneficiary spouse retains discretionary access to distributions for health, education, maintenance, and support

- Donor spouse retains indirect access as long as they remain married to the beneficiary spouse

- Can include children and grandchildren as additional beneficiaries, enabling multi-generational planning

- Assets in a properly structured SLAT receive creditor protection since they are not personal assets

- With the $15M federal exemption, couples can now move up to $30M into SLATs — potentially enough to shield an entire family estate

Critical Risk: The Reciprocal Trust Doctrine

Both spouses may want to establish SLATs for each other’s benefit, effectively allowing each to access the other’s trust. However, the IRS applies the Reciprocal Trust Doctrine to unwind trusts that are ‘substantially similar’ — treating the assets as if each spouse created a trust for themselves, pulling them back into each estate (Fidelity, 2026).

To avoid this, dual SLATs must differ in meaningful ways:

- Created at different times (ideally separate tax years)

- Funded with different asset types (e.g., one with securities, one with real estate)

- Different trustees, different distribution standards, different beneficiary provisions

- Different terms — e.g., one trust for spouse only; one trust for spouse and children

Important: There is no statutory ‘safe harbor’ for dual SLATs. A court makes the final determination. Work with experienced trust and estate counsel (Knox Law, 2026).

SLAT Limitation: No Step-Up in Basis

Strategy 3: Managing the State Estate Tax 'Cliff'

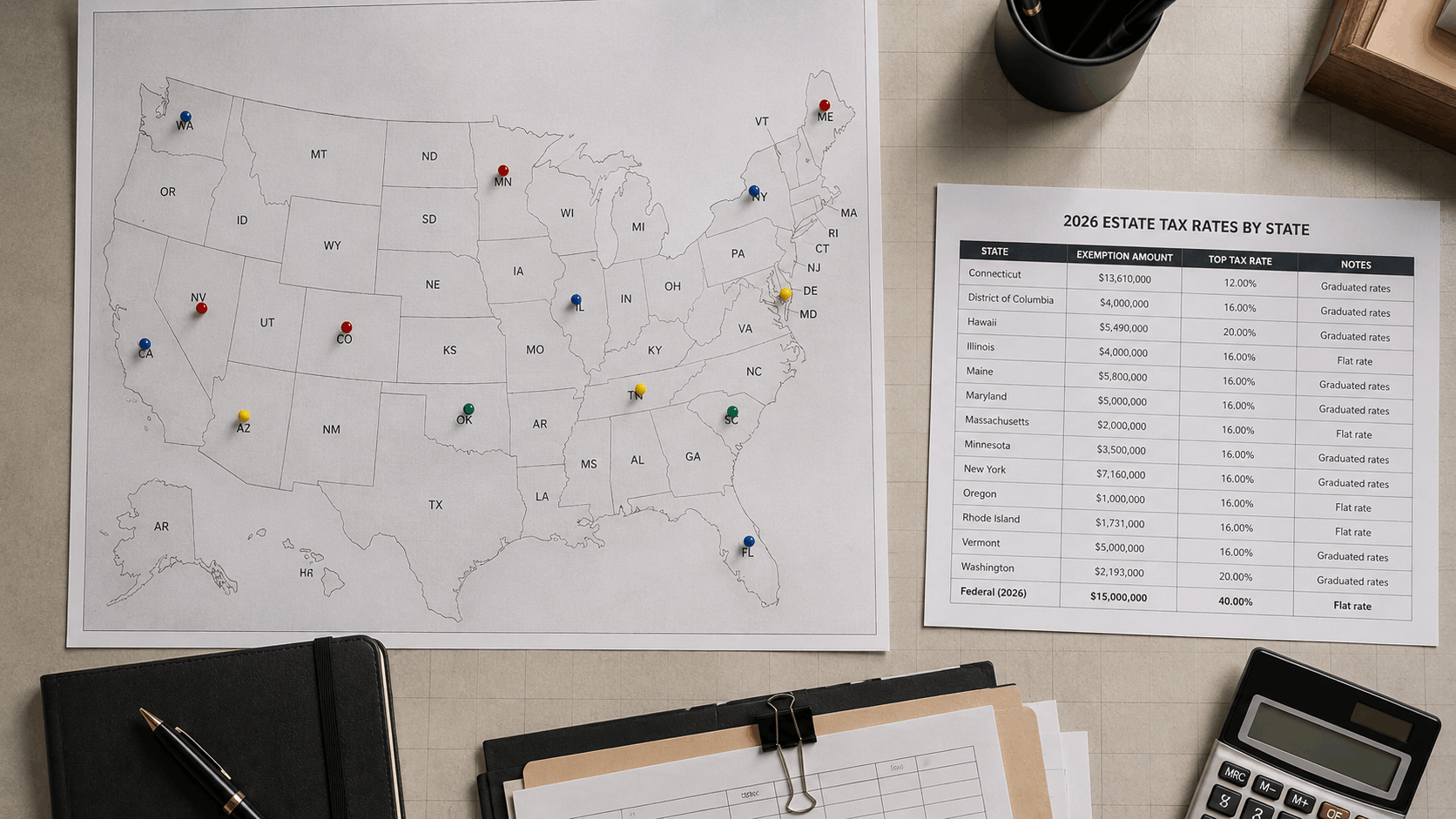

While federal exposure may be reduced or eliminated for many families, 12 states and the District of Columbia still impose their own estate taxes — often with much lower exemptions and no inflation indexing. Your zip code matters as much as your net worth.

| State | 2026 Exemption | Top Rate | Notable Feature |

|---|---|---|---|

| Oregon | $1,000,000 | 16% | Lowest in the U.S. |

| Massachusetts | $2,000,000 | 16% | CLIFF STATE: tax applies to full estate if exceeded |

| Rhode Island | ~$1,730,000 | 16% | Second-lowest exemption nationally |

| New York | $7,350,000 | 16% | CLIFF STATE: 105% rule; no portability |

| Illinois | $4,000,000 | 16% | CLIFF STATE: tax applies to full estate |

| Washington | ~$2,193,000 | 20% | Highest state rate in the country |

| Minnesota | $3,000,000 | 16% | No portability between spouses |

| Maryland | $5,000,000 | 16% | Has BOTH estate and inheritance tax |

Sources: TaxCompare.org (2026); NY Dept. of Taxation and Finance (2026)

The New York Cliff: A Case Study

New York’s estate tax is one of the most punishing in the country due to its ‘cliff’ mechanism. In 2026, the NY exemption is $7,350,000. If an estate exceeds this by less than 5% — i.e., it is between $7,350,001 and $7,717,500 — the estate pays tax only on the excess. But if it exceeds $7,717,500 (105% of the exemption), the entire exemption disappears and the full estate is taxed from dollar one (Twomey Latham, 2026; NY Dept. of Taxation, 2026).

Example: A $7.4 million estate in New York — just $50,000 over the threshold — would owe more than $136,000 in NY state estate tax. That represents an effective marginal rate of over 250% on that final $50,000. This is not a rounding error — it’s a planning failure (Twomey Latham, 2026).

Key State Planning Strategies

- Gifting to the Threshold: Make annual gifts or tactical charitable contributions to reduce the gross estate below the state trigger before death

- Marital Bypass / Credit Shelter Trusts: NY does not allow portability between spouses; a bypass trust at the first death can lock in both spouses’ $7.35M exemptions

- Formula ‘Santa Clause’ Charitable Gifts: Draft your will with a clause that donates to charity any estate value above the NY threshold — but only if the charitable deduction exceeds the tax that would be owed

- NY 3-Year Clawback Rule: Unlike the federal system, NY adds back gifts made within 3 years of death into the state estate calculation. Plan accordingly.

- Relocation Consideration: For clients whose estates substantially exceed state thresholds, domicile planning (e.g., moving to Florida or Texas) can eliminate state estate tax exposure

Answer Block:

New York State imposes its own estate tax with a 2026 exemption of $7,350,000 — far below the $15 million federal threshold. New York is a ‘cliff state’: if an estate exceeds 105% of the exemption (i.e., exceeds $7,717,500 in 2026), the entire state exemption is forfeited and the whole estate is taxed. New York does not allow portability of the state exemption between spouses. Gifts made within 3 years of death are added back into the state estate for tax purposes, making early planning critical.

Strategy 4: Portability vs. GST Planning — A Critical Distinction

How Portability Works

The GST Exemption Is NOT Portable

- Portability: Transfers unused estate/gift tax exemption to surviving spouse. REQUIRES timely Form 706 filing.

- GST Exemption: Applies to generation-skipping transfers. NOT portable. Must be used at first death via a properly structured trust.

- Reverse QTIP Election: One advanced technique is using a reverse Qualified Terminable Interest Property (QTIP) trust to preserve the first spouse’s GST exemption for grandchildren.

Planning action: If the first spouse to die does not have a Dynasty or GST Trust in their estate plan, consult with counsel immediately. The missed exemption — currently $15 million — cannot be recovered.

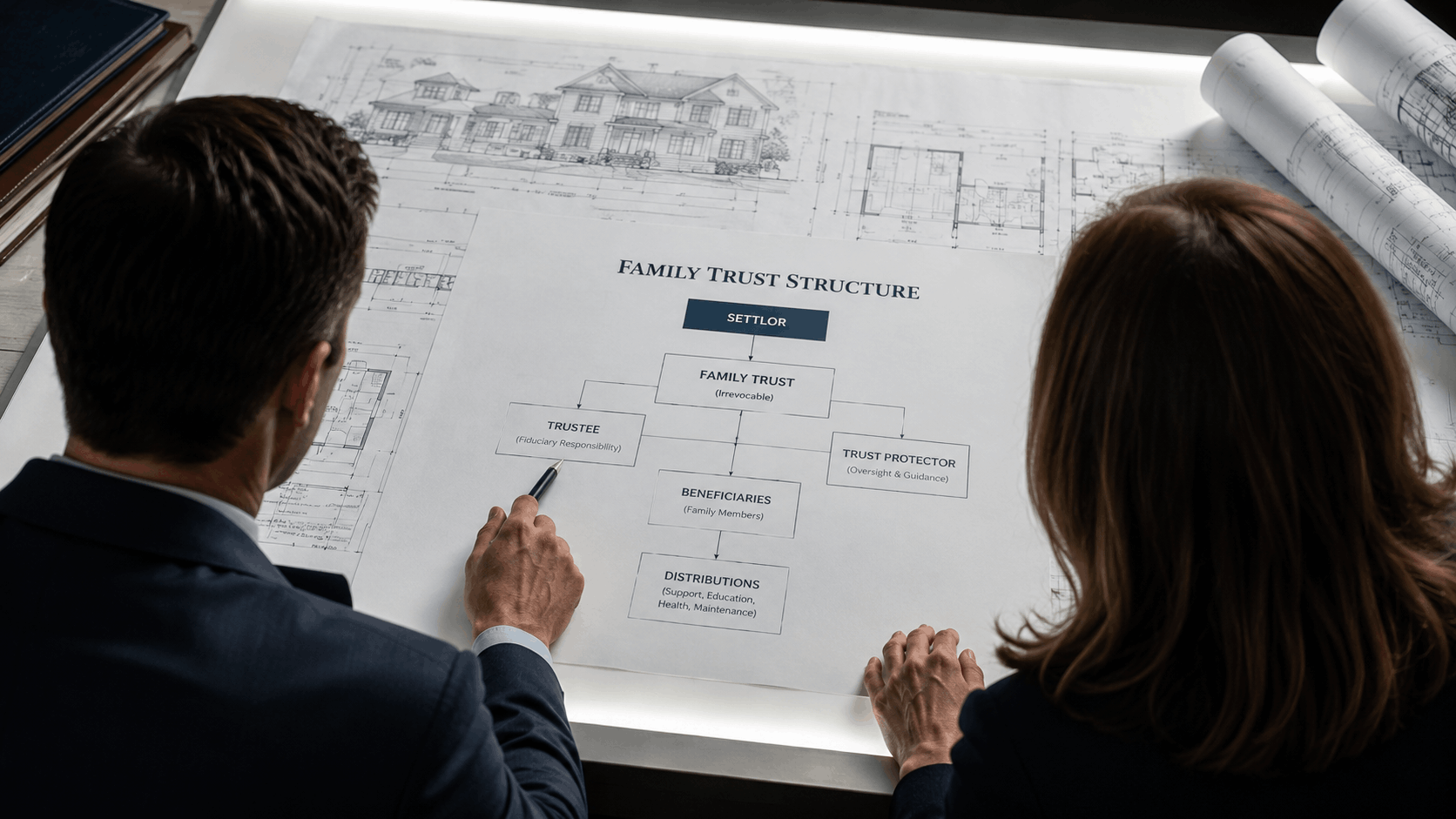

Strategy 5: Dynasty Trusts — The Multi-Generational Tax Shield

Core Mechanics

- Assets placed in the trust are removed from the grantor’s taxable estate immediately

- The trust is allocated the grantor’s GST exemption, shielding all distributions to grandchildren and beyond

- Beneficiaries (children, grandchildren) receive income and principal distributions based on trustee discretion under HEMS standard (Health, Education, Maintenance, Support)

- Assets within the trust remain protected from beneficiaries’ creditors and divorce proceedings

- At each beneficiary’s death, trust assets continue to the next generation — rather than being taxed again as part of that beneficiary’s estate

State Selection for Dynasty Trusts

Not all states are equal for dynasty trusts. States like Alaska, Nevada, Delaware, and South Dakota have abolished or extended the ‘Rule Against Perpetuities,’ allowing dynasty trusts to run indefinitely. These states also tend to have strong asset protection laws and no state income tax on trust income — making them preferred domiciles for the trust situs (Peak Trust, 2026).

The Power of Compounding Inside a Dynasty Trust

Consider a $15 million dynasty trust growing at 7% annually. After 30 years (one generation), the trust holds approximately $114 million — all outside anyone’s taxable estate. After 60 years (two generations), it approaches $870 million. Every dollar of estate tax saved at the initial transfer compounds for future generations.

Additional Strategies for the 2026 Landscape

Annual Gifting Programs

GRATs (Grantor Retained Annuity Trusts)

Review Existing Trusts for Formula Clause Issues

Frequently Asked Questions

1. Did the One Big Beautiful Bill Act make the $15M estate tax exemption truly permanent?

The OBBBA permanently increased the federal estate and gift tax exemption to $15 million per individual, effective January 1, 2026 — with no automatic sunset date. Starting in 2027, the amount will be adjusted for inflation. However, ‘permanent’ in tax law always carries an asterisk: a future Congress could amend the exemption. Estate attorneys widely advise acting within the next few years while the rules are stable (Pierce Atwood, 2025; Morgan Lewis, 2025).

2. What is the New York estate tax ‘cliff’ and how do I avoid it?

New York’s estate tax cliff activates when an estate exceeds 105% of the state exemption ($7,717,500 in 2026). At that point, the entire $7.35M exemption disappears — meaning the full estate is taxable, not just the excess. Strategies to avoid the cliff include gifting assets to fall below the threshold, funding bypass trusts at the first spouse’s death, and including formulaic charitable provisions that trigger only when cost-effective (Twomey Latham, 2026; NY Dept. of Taxation, 2026).

3. What is an IDGT and why is it still relevant with a $15M exemption?

An Intentionally Defective Grantor Trust (IDGT) is an irrevocable trust that is ‘defective’ for income tax purposes but effective for estate tax purposes. By selling a high-growth asset to an IDGT for a promissory note at the AFR, the grantor freezes the asset’s estate value and shifts all future appreciation to heirs tax-free. This strategy matters for any family with estate assets well above $15 million, or who expects significant asset appreciation (Fidelity, 2026; RSM, 2024).

4. Can both spouses each set up a SLAT?

Yes, but with significant caution. If both spouses create SLATs for each other’s benefit, the IRS may apply the Reciprocal Trust Doctrine to unwind both trusts — effectively treating each as having created a trust for themselves and pulling all assets back into each estate. To avoid this, dual SLATs must differ meaningfully: different timing, different assets, different trustees, different distribution standards, and different beneficiary structures (Schwab, 2026; Fidelity, 2026).

5. Is the GST exemption portable like the estate tax exemption?

No. Unlike the estate and gift tax exemption, the GST exemption cannot be transferred from a deceased spouse to the survivor. If the first spouse to die does not allocate their $15 million GST exemption to a properly structured trust (typically a dynasty trust or GST trust), that exemption is permanently lost. This is one of the most consequential oversights in HNW estate planning (Associated Bank, 2026; Fidelity, 2026).

6. Should I revisit my estate plan even if I’m under the $15M threshold?

Yes, especially if you live in one of the 12 states with a separate estate tax, if your estate plan contains formula clauses tied to the federal exemption, or if you created aggressive gifting strategies specifically designed to beat the now-averted 2026 sunset. Plans drafted in 2022–2024 may no longer operate as intended (BNY Wealth, 2026; Carolina Financial & Estate Planning, 2025).

7. How often should HNW families review their estate plans?

Estate planning professionals recommend a full review every 3–5 years, or immediately following any major life event: death of a family member, significant asset acquisition, relocation across state lines, major change in asset values, or new legislation. The OBBBA constitutes such a trigger for virtually all HNW families with existing plans (Carolina Financial & Estate Planning, 2025; Pierce Atwood, 2025).

Works Cited

Associated Bank. “How Does the Generation-Skipping Transfer Tax Work.” AssociatedBank.com. March 4, 2026. https://www.associatedbank.com/education/articles/personal-finance/financial-planning/generation-skipping-transfer-tax

BNY Wealth. “How the One Big Beautiful Bill’s $15M Estate Exemption Reshapes Multigenerational Giving.” BNY.com. March 30, 2026. https://www.bny.com/wealth/global/en/insights/qa-how-the-one-big-beautiful-bills-15m-estate-exemption-reshapes-multigenerational-giving.html

Escalon Services. “The 2026 Estate Tax Changes: What Business Owners Need to Know.” Escalon.services. February 23, 2026. https://escalon.services/blog/taxes/the-2026-estate-tax-changes

Fidelity Investments. “Generation Skipping Transfer Tax (GSTT) Explained.” Fidelity.com. March 12, 2026. https://www.fidelity.com/viewpoints/wealth-management/insights/generation-skipping-transfer-tax

Fidelity Investments. “Intentionally Defective Grantor Trusts.” Fidelity.com. March 30, 2026. https://www.fidelity.com/viewpoints/wealth-management/insights/intentionally-defective-grantor-trusts

Fidelity Investments. “Protect Assets with a SLAT.” Fidelity.com. January 21, 2026. https://www.fidelity.com/learning-center/wealth-management-insights/protect-assets-with-a-SLAT

Fiduciary Trust. “Spousal Lifetime Access Trusts.” FiduciaryTrust.com. January 22, 2026. https://www.fiduciary-trust.com/insights/spousal-lifetime-access-trusts/

Internal Revenue Service. “IRS Releases Tax Inflation Adjustments for Tax Year 2026.” IRS.gov. October 9, 2025. https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

Knox Law Firm. “Spousal Lifetime Access Trusts (SLATs).” KMGSlaw.com. February 13, 2026. https://www.kmgslaw.com/knox-law-institute/publications/spousal-lifetime-access-trusts-slats-not-just-for-the-rich-and-famous

Morgan Lewis. “Estate Tax Alert: New $15 Million Federal Exemption Becomes Law.” MorganLewis.com. August 21, 2025. https://www.morganlewis.com/pubs/2025/08/estate-tax-alert-new-15-million-federal-exemption-becomes-law

New York Department of Taxation and Finance. “Estate Tax — New York State Exclusion Amounts.” Tax.NY.gov. 2026. https://www.tax.ny.gov/pit/estate/etidx.htm

Peak Trust Company. “What is a Dynasty Trust.” PeakTrust.com. January 28, 2026. https://peaktrust.com/what-is-a-dynasty-trust/

Pierce Atwood LLP. “The One Big Beautiful Bill Act and Estate Planning.” PierceAtwood.com. 2025. https://www.pierceatwood.com/alerts/one-big-beautiful-bill-act-and-estate-planning-what-you-need-know

RSM US LLP. “Estate Planning Q&A: Sales to Intentionally Defective Grantor Trusts.” RSMus.com. 2024. https://rsmus.com/insights/services/business-tax/sales-to-intentionally-defective-grantor-trusts-explained.html

Charles Schwab. “SLAT Trusts: Estate Planning for Couples.” Schwab.com. 2026. https://www.schwab.com/learn/story/slat-trusts-estate-planning-strategy-couples

TaxCompare. “Estate and Inheritance Tax by State: The Complete 2026 Map.” TaxCompare.org. March 30, 2026. https://www.taxcompare.org/blog/estate-inheritance-tax-by-state

Twomey Latham. “Avoiding the Cliff: Understanding New York’s Estate Tax.” SuffolkLaw.com. February 5, 2026. https://www.suffolklaw.com/avoiding-the-cliff-understanding-new-yorks-estate-tax/

U.S. Bank. “Dynasty Trust: Planning for Future Generations.” USBank.com. January 16, 2026. https://www.usbank.com/wealth-management/financial-perspectives/trust-and-estate-planning/dynasty-trust.html