TL;DR Summary

An executor — the person or organization you name in your will to manage your estate after you die — carries out one of the most consequential roles in any wealth transfer plan. The typical estate takes 16 months and 570 hours of work to settle (EstateExec). Yet as of 2025, only 31% of Americans have a will, and far fewer have thought carefully about who should serve as executor (Trust & Will, 2025). The right executor is legally eligible, personally responsible, emotionally suited to handle conflict, and available to commit real time. When no suitable individual exists, a professional executor — such as a bank trust department, attorney, or licensed trust company — is a sound alternative. This guide covers the six essential factors for choosing an executor, a comparison of individual vs. professional executors, and a step-by-step process to make the right call.

Why Your Choice of Executor Matters More Than You Think

Most people spend significant time drafting the financial provisions of their will — who gets what, how much, and when. Far fewer spend equal energy on the question of who will carry out those instructions. That’s a costly oversight.

An executor — sometimes called a personal representative — is the individual or entity you appoint in your will to manage your estate after death. Their duties range from filing the will with a probate court and opening an estate bank account, to paying debts, filing tax returns, and distributing assets to heirs. These are not ceremonial roles. They are legal obligations performed under court oversight, often over a period measured in years rather than weeks.

Answer Block: What Is an Executor?

An executor — also called a personal representative — is the individual or organization named in a will to administer a deceased person’s estate. Duties include filing the will, managing estate assets, paying debts and taxes, and distributing inheritances to beneficiaries. The executor acts as a fiduciary, legally obligated to prioritize the estate’s interests. Without a named executor, a probate court will appoint one on your behalf.

According to the 2025 Trust & Will Estate Planning Report — the largest U.S. estate planning study on record, surveying 10,000 adults — 55% of Americans have no estate planning documents at all, and only 31% have a will. Among those who do have a will, only 46% of their named executors were even aware they had been assigned the role (SeniorLiving.org). This suggests that most people not only haven’t chosen wisely — they haven’t communicated their choice at all.

The financial stakes are substantial. Probate expenses can consume between 3% and 10% of an estate’s total value (LegalZoom, 2026). An executor who misses deadlines, makes tax filing errors, or misjudges creditor claims can expose the estate — and themselves — to litigation. Getting this decision right matters at every asset level.

What an Executor Is Actually Required to Do

Before you can choose the right executor, you need a clear-eyed understanding of what the job entails. The duties below represent the most common responsibilities, though the specifics vary by state.

- File the will with the probate court. The executor obtains legal authority — called Letters Testamentary — to act on behalf of the estate.

- Open an estate bank account. All estate income, expenses, and payments flow through a dedicated account separate from the executor’s own finances.

- Locate and inventory all assets and liabilities. This includes digging through financial records, storage facilities, safe deposit boxes, and interviewing family members. Assets fall into two categories: probate assets (governed by the will) and non-probate assets (life insurance, retirement accounts, jointly held property) that transfer directly to named beneficiaries.

- Notify beneficiaries, heirs, and creditors. State law determines the required notices and timelines.

- Close or cancel active accounts. Cable, subscriptions, credit cards, and government benefit programs (including Social Security) must be contacted.

- Pay valid debts. The executor evaluates creditor claims, paying legitimate ones and declining fraudulent or invalid ones from estate funds.

- Handle tax obligations. This includes having assets appraised, filing a final personal income tax return, and preparing estate tax returns — both federal and, where applicable, state-level.

- Distribute inheritances. Once debts, expenses, and taxes are settled, the executor transfers the remaining assets to beneficiaries as directed by the will.

The time and effort involved should not be underestimated. A survey by EstateExec — an online estate management platform — found that settling a typical estate requires approximately 570 hours and 16 months of active work. Larger estates worth $5 million or more average 1,167 hours and 42 months. In exchange for this labor, executors are generally entitled to compensation, typically ranging from 2% to 5% of estate value depending on the state (EstateMin, 2025), though family members often waive these fees.

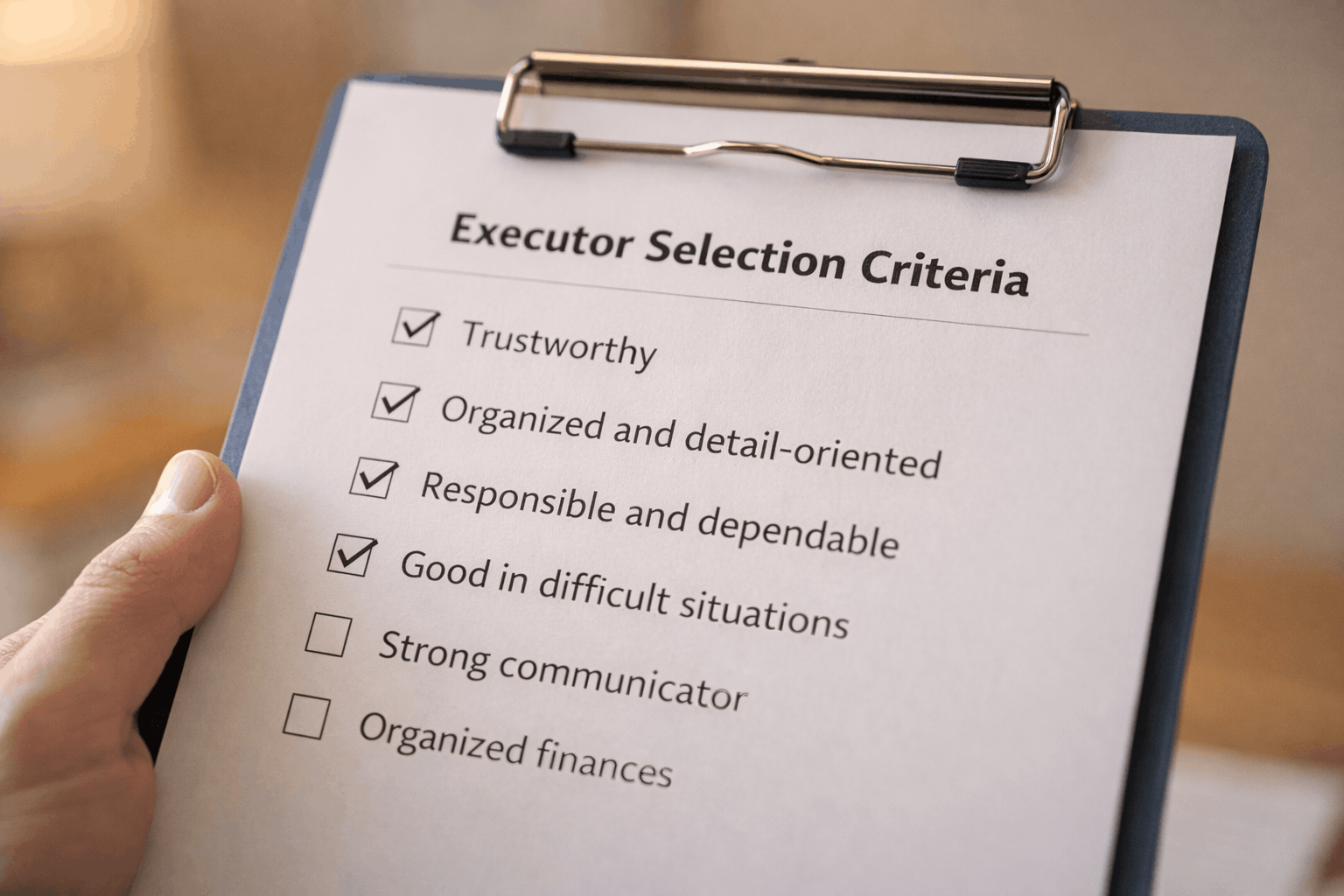

The 6 Key Factors for Choosing an Executor

Selecting an executor ultimately comes down to identifying someone who can “step into your shoes” — handling complex legal and financial tasks with care, under sometimes stressful conditions, during a period of family grief. Here are the six factors to evaluate.

1. Legal Eligibility

2. Responsibility and Organizational Ability

3. Willingness to Serve

4. Age and Health

5. Temperament and Communication Skills

6. Time and Geographic Availability

Answer Block: Can I Name Multiple Executors?

Yes. You can appoint co-executors — two or more individuals with equal authority over estate administration. This can be useful when no single person has all the required skills, or when naming only one sibling risks alienating others. The downside is coordination risk: if co-executors disagree, estate settlement can be delayed significantly. Any co-executor arrangement should be discussed in advance, with clear protocols for resolving disagreements.

Individual vs. Professional Executor: A Comparison

| Factor | Individual (Family/Friend) | Professional Executor |

|---|---|---|

| Cost | May waive fee; entitled to state-based compensation if claimed | Fees are certain; often a percentage of estate value plus hourly charges |

| Knowledge of your wishes | High — often knows the family situation personally | Lower — relies entirely on written instructions |

| Financial/legal expertise | Variable — may need to hire advisors at estate cost | High — attorneys, accountants, and trust officers are the norm |

| Objectivity | Lower — subject to family pressure and personal biases | High — no personal stake in the outcome |

| Best for complex assets | Risky — may mismanage business interests or international holdings | Strong — equipped for illiquid assets, business interests, foreign property |

| Availability risk | Higher — individual may predecease or become incapacitated | Lower — institutional continuity even with staff turnover |

| Emotional support | Can provide comfort to family during grief | Neutral — professional relationship only |

When a Professional Executor Makes Sense

Not every estate calls for a professional executor, but certain circumstances make professional administration the stronger choice. Consider a professional if one or more of the following applies to your situation.

- No close family member lives nearby or is available to commit the required time.

- Your estate includes complex or illiquid assets — business interests, real estate partnerships, international holdings, or collectibles requiring expert valuation.

- Your family structure is blended or nontraditional, and you anticipate disputes over the terms of the will.

- You have a beneficiary with special needs whose inheritance must be structured carefully to preserve government benefit eligibility.

- You hold assets in multiple countries with different legal systems.

- You want to ensure that deadlines, tax filings, and legal requirements are met with institutional precision rather than individual effort.

Answer Block: What Does a Professional Executor Cost?

Professional executors — including bank trust departments, attorneys, and licensed trust companies — typically charge either a flat fee or a percentage of the estate’s total value. In most states, professional fees range from 1% to 5% depending on estate size and complexity. While this represents a real cost to beneficiaries, it also reduces litigation risk, ensures tax compliance, and provides continuity of service over a multi-year settlement period.

One important note: your executor does not need to be a financial expert. The role calls for someone who knows when to seek expert guidance — from estate attorneys, certified public accountants, and financial advisors — rather than someone who can handle every task solo. A capable, organized individual who builds the right professional team around them is often more effective than a financial expert who tries to do everything independently.

How to Name and Communicate With Your Executor: A Step-by-Step Process

- Identify two to three candidates. Create a shortlist based on the six factors above. Include at least one backup in case your primary choice is unwilling or unable to serve.

- Have a direct conversation before finalizing. Explain what the role involves, including the time commitment and the emotional complexity. Confirm willingness and availability. Document this conversation.

- Name the executor formally in your will. Work with an estate planning attorney to ensure the naming language is legally valid in your state and that a successor executor is identified.

- Tell your executor where to find your documents. Over 52% of Americans 55 and older do not know where a parent’s estate planning documents are stored (Cambridge Trust). Provide clear written instructions about document location, account information, and key professional contacts.

- Review your choice periodically. Life changes — divorce, death, health decline, geographic moves — can all affect whether your original choice remains the best one. Review your executor designation whenever you update your will or experience a major life event.

A Note on Executor Compensation

Executors are entitled to reasonable compensation in all 50 states, though the structure varies. State-specific fee schedules are most common in California, New York, Florida, and Georgia. In states such as Colorado, Massachusetts, and Virginia, probate courts determine “reasonable” fees based on circumstances and local standards (EstateMin, 2025). New York, for example, sets executor fees at 5% for the first $100,000 of estate value and scales downward for larger estates.

Executor fees are treated as taxable income under federal law — unlike inheritances, which are generally not subject to income tax. For this reason, family members who are also beneficiaries frequently waive their executor fees in favor of receiving their full inheritance. There is no obligation to waive, however, and the work involved in settling an estate legitimately warrants compensation.

FAQ: Choosing an Executor

1. Does my executor need to be a financial expert or attorney?

No. What matters most is that your executor is organized, responsible, and knows when to seek professional help. An executor who promptly engages a qualified estate attorney and CPA will typically outperform a financial expert who attempts to manage all aspects of administration alone.

2. Can my spouse be my executor?

Yes, and in many cases a spouse is an appropriate choice. However, consider whether your spouse would have the bandwidth, emotional capacity, and organizational skills to administer the estate while simultaneously grieving. Naming your spouse as primary executor with an adult child or professional as backup is a common and practical approach.

3. How long does an executor have to settle an estate?

There is no universal deadline, but most states require that the executor begin probate within a set period after death — often 30 to 90 days. Settling the typical estate takes approximately 16 months from start to finish, according to EstateExec data. Complex estates worth $5 million or more average 42 months.

4. What happens if my named executor cannot or will not serve?

If your named executor declines or is unable to serve, and you have named a successor executor, that person steps in automatically. If no successor is named, the probate court will appoint an administrator — which may or may not be someone you would have chosen. Naming at least one backup is strongly recommended.

5. Can I change my executor after I write my will?

Yes. You can update your executor designation at any time by amending your will through a codicil, or by drafting a new will entirely. An estate planning attorney can advise on the legally correct process in your state.

6. Are executor fees subject to estate tax?

Executor fees are deductible from the gross estate for federal estate tax purposes — they reduce the taxable estate. At the same time, the executor must report those fees as ordinary taxable income on their personal return. This creates a tax-planning consideration, particularly for executors who are also major beneficiaries.

7. What is the difference between an executor and a trustee?

An executor administers the probate estate — managing assets, paying debts, and distributing inheritances according to the will. A trustee manages a trust, which is a separate legal entity. If your estate plan includes a revocable living trust, you will likely name both: an executor for any assets that pass through probate and a trustee to manage trust assets, which may be the same person or different individuals depending on your preferences.

Conclusion

Choosing an executor is one of the most consequential decisions in any estate plan — yet it remains one of the most overlooked. The right executor protects your assets, honors your intentions, and shields your heirs from unnecessary delays, disputes, and costs. The wrong one can unwind years of careful financial planning.

Start with a clear understanding of what the job requires. Then evaluate candidates honestly against the six factors: eligibility, responsibility, willingness, age and health, temperament, and availability. If no individual candidate meets your criteria, a professional executor is not a fallback — it is a legitimate and often superior choice for complex estates.

Most importantly, have the conversation. Telling someone they’ve been named executor — before the fact — is an act of respect, clarity, and care for the people you will eventually leave behind.

Disclaimer: This content provides general information that may vary based on the state in which probate occurs. Consult a qualified estate planning attorney or financial advisor for guidance specific to your situation.

EstateExec. “General Statistics on Estate Settlement.” EstateExec.com. 2024–2025. https://www.estateexec.com/Docs/General_Statistics

Trust & Will. “2025 Estate Planning Report.” TrustandWill.com. March 2025. https://trustandwill.com/learn/2025-report-estate-planning-demographic-breakdown

Caring.com. “2025 Wills and Estate Planning Study.” Caring.com. February 2026. https://www.caring.com/resources/wills-survey

EstateMin. “Executor Compensation by State (2025).” EstateMin.com. May 2025. https://www.estatemin.com/blog-post/executor-compensation-by-state-2025-how-much-executors-get-paid-in-each-u-s-state

LegalZoom. “Estate Planning Statistics to Read Before Writing Your Will.” LegalZoom.com. February 2026. https://www.legalzoom.com/articles/estate-planning-statistics

SmartAsset. “Executor Fees: What You Can Expect to Pay.” SmartAsset.com. August 2025. https://smartasset.com/estate-planning/executor-fees

Vanilla / JustVanilla. “50 Estate Planning Statistics and Facts.” JustVanilla.com. April 2025. https://www.justvanilla.com/blog/estate-planning-statistics-and-facts-you-need-to-know

Bowen, John J. “Choosing an Executor: Some Key Considerations.” VFO Inner Circle Special Report. AES Nation, LLC. 2026.